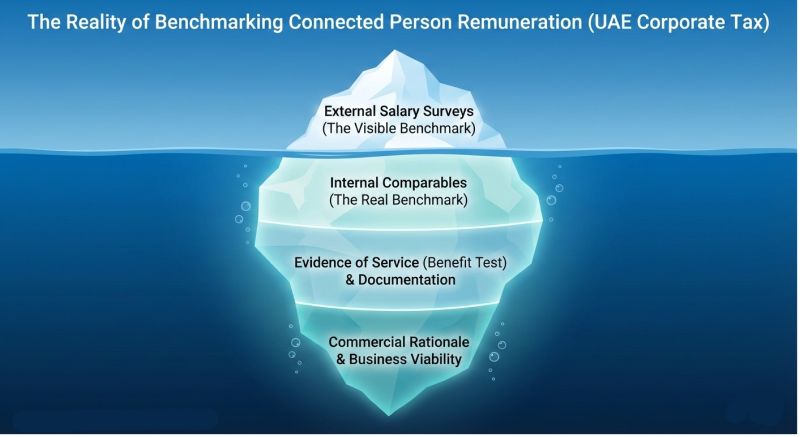

The "Salary Survey" Trap: Why Benchmarking Fails UAE Directors

To comply with Article 36 of the UAE Corporate Tax Law, I see a dangerous trend emerging: the blind reliance on "Salary Surveys" to justify Connected Person remuneration.

The “Salary Survey” Trap: Why Benchmarking Fails UAE Directors

To comply with Article 36 of the UAE Corporate Tax Law, I see a dangerous trend emerging: the blind reliance on “Salary Surveys” to justify Connected Person remuneration. The textbook tells you to use the CUP method. It sounds perfect on paper. You find a survey, see that a “General Manager” in Dubai earns AED 60k/month, and voila—your deduction is safe. But let’s be real. In the UAE’s private sector, comparing job titles is often an exercise in comparing apples to oranges. A “General Manager” in a family-owned trading house is not the same as a “General Manager” in a multinational conglomerate. The operational realities, risks, and authority levels are vastly different. So, if external data is distortive, do we fall back to the TNMM?

The TNMM Trap: Profit vs. Price

Using TNMM to justify a salary is technically a mismatch. TNMM measures net margins, not prices. If you argue, “Our company makes a healthy 15% net margin even after paying the Director AED 2M, so the salary is fine,” you are walking into a trap.

The FTA argues: “Your margin should have been 25%. The excessive salary didn’t facilitate business; it stripped out your super-profits.”

TNMM hides the granular reality of the expense. It is a “masking” tool, not a pricing tool.

A Better Way: The Corroborative Approach

Broad View:

-

The Qualitative Foundation (The “Benefit Test”)

Before we talk numbers, we talk value. Forget the benchmark for a second—does the paper trail exist?

show me the board minutes showing the decisions, this director made?

Where is the evidence of their strategic intervention?

If you can’t prove they worked, the “market rate” for their salary is zero.!!! -

The “Internal CUP”

The most reliable data is in your own payroll.

Instead of comparing your Director to a stranger in a survey, compare them to your own unconnected senior staff.

Ex: If your employed, non-connected Sales Director earns AED 40k, and your Connected Owner-Director earns AED 200k for a similar workload, you have a gap that no external survey can bridge.

Defense: If the gap is small (e.g., 20% premium for higher responsibility), it is internally defensible. -

TNMM as a “Sanity Check” Only

Use TNMM only as a secondary layer. Don’t use it to set the price; use it to prove that the salary didn’t erode the commercial viability of the business. It shows that the company remains healthy and tax-generative, proving the expense wasn’t a profit-shifting scheme.

The Bottom Line, In the UAE context, specificity beats generality.

A generic recruitment survey is weak evidence. A specific, internally consistent logic—backed by proof of service—is strong evidence.

Don’t let “standard practice” expose you to audit risks. The FTA isn’t looking for a perfect salary match in a database; they are looking for commercial rationality.

Build your defense on that