UAE TP Framework-Basic Thresholds

For businesses operating in the UAE, Transfer Pricing (TP) has evolved from a best-practice recommendation to a mandatory compliance pillar under the Corporate Tax regime. Below is an overview of the regulatory requirements, documentation thresholds, and reporting obligations.

- The Legislative Framework:

The UAE TP regime is governed by Federal Decree-Law No. 47 of 2022 and supported by Ministerial Decision No. 97 of 2023.

Arm’s Length Principle (Article 34): All transactions between Related Parties and Connected Persons must be priced as if the parties were independent.

Related Parties (Article 35): Entities or individuals with common control or ownership (50% or more).

Connected Persons (Article 36): Owners, directors, or officers of the business and their relatives. Payments to these individuals must reflect market value and be incurred solely for business purposes.

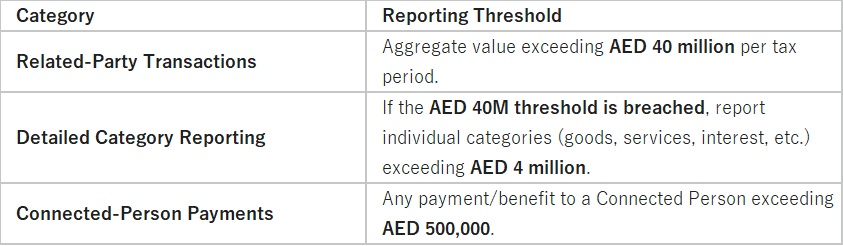

- Reporting & Documentation Thresholds

Compliance is determined by your revenue and the nature of your transactions. Note that while specific documentation thresholds exist, all related-party transactions remain subject to the Arm’s Length Principle regardless of size. ( Basically Threshold is Zero!! Every Dirham Needs to Follow Arm’s Length Principle)

A. Transfer Pricing Disclosure Form (TPDF) : The TPDF is a mandatory filing submitted via the EmaraTax portal alongside your annual Corporate Tax Return.

B. Master File & Local File : These documents provide the FTA with a technical justification for your pricing methodology. They must be prepared contemporaneously (at the time of the transaction) and provided to the FTA within 30 days of a formal request.

Local File Requirement: Applicable if your standalone UAE revenue is AED 200 million or more.

Master File Requirement: Applicable if you are a constituent entity of an MNE group with total consolidated group revenue of AED 3.15 billion or more.

- Compliance and Penalties: Non-compliance in the UAE is subject to a rigorous penalty framework, particularly following recent updates to tax procedures.

Administrative Penalties: Failure to provide requested documentation (Local/Master File) within the 30-day window can result in fines starting from AED 10,000.

Tax Adjustments: If the FTA rejects your pricing methodology during an audit, it will perform a transfer pricing adjustment. This increases your taxable income and triggers a 9% corporate tax liability on the adjustment, plus potential late payment interest.

Voluntary Disclosures: If you identify errors after filing, submitting a Voluntary Disclosure prior to an audit notification can significantly reduce penalties compared to post-audit assessments.

Summary Checklist for Finance Leaders:

Annual TPDF Filing: Ensure your accounting system tracks related-party transactions by category to determine if you exceed the AED 40M / 4M / 500k thresholds for the disclosure form.

Contemporaneous Documentation: Even if you fall below the Local/Master File threshold, maintain internal records (ex:invoices, contracts, and market analysis) to justify your pricing.

Governance: For “Connected Persons” (directors/owners), ensure all payments are documented as “market value” for “business purposes” to avoid denial of tax deductions.

Audit Readiness: If your annual revenue exceeds the AED 200 million mark, ensure your Master/Local files are updated annually and ready for production within the 30-day FTA window.

*For More Detailed Discussion on Compliance Thresholds…Do Write to us at sbhargava{at]ca-bhargava[dot]com *